Understanding Switzerland’s social security system starts with Pillar 1, which, for the purposes of this article, we can consider the Swiss equivalent of U.S. Social Security.

For U.S. citizens living and working in Switzerland, Pillar 1 is more than a basic retirement benefit. It’s a foundational layer of your cross-border financial plan that interacts directly with U.S. expatriate taxation, long-term retirement strategy, and estate planning decisions.

Whether you’re a high-earning professional on assignment, building a career in Switzerland, or planning retirement in Switzerland, understanding how Pillar 1 works and how it fits into your broader U.S. financial picture is essential.

This article is part of a three-part series covering:

- Pillar 1 (state pension)

- Pillar 2 (occupational pension)

- Pillar 3 (private savings)

Last updated: May 2026

The Swiss Pension System, in Context

Switzerland’s pension system is built on a three-pillar structure, designed to balance:

- Basic income security (Pillar 1)

- Employer-based retirement savings (Pillar 2)

- Voluntary wealth accumulation (Pillar 3)

While this may sound similar to the U.S. system, the mechanics (and especially the tax treatment) are very different.

It’s also important to understand that, like many developed countries, Switzerland is actively reforming its pension system in response to demographic pressure. Current policy discussions (including AHV 2030 reform proposals) focus on long-term sustainability without dramatically increasing the retirement age.

For U.S. expats, this means that you’re planning inside a system that is notoriously stable but also evolving.

What Is Pillar 1 in Switzerland?

Pillar 1 is Switzerland’s mandatory state pension system, known as:

- AHV (German acronym)

- AVS (French acronym)

- OASI (English acronym)

It is administered by cantonal compensation offices and designed to cover basic living expenses in retirement or disability.

Pillar 1 includes:

- Old-Age and Survivors’ Insurance (AHV/AVS): Retirement income and survivor benefits

- Disability Insurance (IV/DI): Income support if you are unable to work

- Supplementary Benefits (EL): Additional support if minimum living costs are not met

New in 2026: The 13th AHV/AVS Pension Payment

In recent Swiss social security news, it was announced that, beginning in 2026, Switzerland will introduce a 13th annual AHV/AVS payment, following a national referendum passed in March 2024.

For eligible retirees, this means:

- An additional month of state pension income each year

- Typically paid as a lump sum (expected in December)

What this means for U.S. expats: This applies only if you qualify for a Swiss state pension through contributions.

It does not apply if:

- You’ve never worked in Switzerland

- You rely solely on U.S. Social Security or private assets

From a planning perspective, this change:

- Increases Swiss taxable income

- May affect U.S. tax exposure depending on your situation

- Should be factored into retirement income projections

Contributing to Pillar 1 (2026 Rates)

Pillar 1 is funded through mandatory contributions.

Employed Individuals

- Total contribution: 10.6% of gross salary

- Split evenly between employer and employee

This covers:

- AHV (retirement)

- Disability Insurance

- Income compensation (EO)

Key Insight for High Earners

Unlike the U.S., Switzerland does not cap income subject to social security contributions.

That means:

- Contributions apply to your full salary

- High earners contribute significantly more over time

Switzerland vs USA Contributions & Tax Treatment

Contributions After Retirement Age

If you continue working beyond the Swiss reference age (65):

- You must still contribute to AHV

- Contributions automatically apply only to income above CHF 16,800/year, however, you may choose to apply contributions to the entire salary if you wish.

Self-Employed and Non-Employed Contributions

- Self-employed: up to 10.0%, with reduced rates at lower income levels

- Non-employed: minimum contribution of CHF 530/year

This is especially relevant for:

- Early retirees

- Spouses who were not the primary earner or who took a career gap

- Wealthy individuals not drawing a salary

How Your Swiss Pension Is Calculated

Your Pillar 1 benefit depends on:

- Total years of contributions (max: 44 years)

- Average lifetime income

- Contribution gaps

2026 Pension Ranges (Estimated)

- Minimum: ~CHF 1,260/month

- Maximum: ~CHF 2,520/month

- Married couples: capped at 150% of max

Missing contribution years will reduce your benefit proportionally.

Swiss vs U.S. Social Security: Key Differences

Here’s where cross-border planning becomes critical.

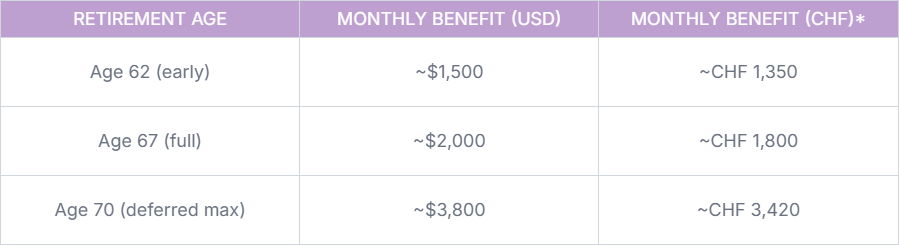

Retirement Age: Switzerland vs U.S.

Switzerland:

- Reference age: 65 (men and women)

- Early withdrawal: up to 2 years

- Deferral: up to 5 years

- Partial withdrawals allowed (20–80%)

United States:

- Full retirement age: 67

- Early: 62

- Deferral increases benefits

U.S. Social Security Benefit Comparison (2026)

.png "U.S. Social Security Benefit Comparison (2026)")

Note that the conversions above assume a 1 USD ≈ 0.90 CHF conversion rate, so figures will likely be a bit lower than what you’re seeing in real time with the volatility in the Middle East and other global events at the time of this writing.

U.S.–Switzerland Totalization Agreement

The totalization agreement helps prevent double contributions when working across both countries.

It allows:

- Coordination of contribution periods

- Eligibility for benefits across systems

However, it does not cover U.S. Medicare.

Swiss Pension Taxation for U.S. Expats

A point to understand: Swiss pensions are generally taxable in the U.S.

This creates several planning layers:

- Foreign income reporting

- Treaty interpretation

- Potential double taxation mitigation

For high earners and retirees, this is where completely unintentional mistakes can become costly. In many cases, working with a professional cross-border advisor can help you spot gaps and planning opportunities – which could ultimately save you a significant amount in the long run.

Early Retirement and Planning Considerations

Switzerland offers more flexibility than the U.S.:

- Partial pension withdrawals

- Continued contributions after early retirement

- Wealth-based contribution calculations

But it’s important to remember that, when it comes to the cross-border space, the price of increased flexibility is often increased complexity.

Why Pillar 1 Alone Is Not Enough

The Swiss social security system has a strong foundation in Pillar 1, but it’s important to recognize that Pillar 1 is intentionally designed to cover basic living expenses only.

- For high earners or affluent retirees:

- It will represent a small portion of total retirement income

Most wealth will sit in: Pillar 2, investment portfolios, and U.S.-based accounts.

Final Considerations for U.S. Expats

Working across the U.S. and Switzerland can create powerful financial opportunities, but it often first reveals inefficiencies.

The key variables include:

- Contribution gaps

- Currency exposure (and managing that risk)

- Tax coordination

- Treaty interpretation

- Investment structure (PFIC risk, navigating net investment income tax, potential Roth conversions, etc.)

The addition of the 13th AHV/AVS payment in 2026 is a reminder of the fact that even “stable” systems evolve, and this means that your plan needs to evolve with them.

How Connected Financial Planning Can Help

At Connected Financial Planning, we work with high-earning U.S. expats and retirees in Switzerland to design integrated, cross-border financial strategies that align both U.S. and Swiss systems.

This includes:

- Coordinating U.S. and Swiss retirement income

- Structuring assets to avoid unnecessary tax exposure

- Planning distributions across multiple jurisdictions

- Navigating treaty complexities with confidence

If you’re building a long-term future in Switzerland or planning to retire here, having a coordinated strategy can make a meaningful difference.

Resources

- Tax Alert – Switzerland: Key Changes from 2025/2026 | EY - Switzerland

- Swiss set priorities for pension reform without raising retirement age - SWI swissinfo.ch

- OASI contributions

- Contribution and Benefit Base – SSA

- AHV/AVS reform: What will change for me? – Swiss Life

- What the Data Says About Social Security – Pew Research Center

- 2026 Cost-of-Living Adjustment (COLA) Fact Sheet | News | SSA

- Totalization Agreement with Switzerland

- AXA - Pillar 1

Meet the Author

Arielle Tucker is a Certified Financial Planner™ and IRS Enrolled Agent with Connected Financial Planning. She's spent over a decade working with US expats on US tax and financial planning issues. She is passionate about working with US expats and their families to help secure a financial future that is reflective of their core values. Arielle grew up in New York and has lived throughout the US, Germany, and Switzerland.