Understanding Swiss cantons is essential to successfully navigating and planning for both Swiss taxes and your cross-border tax situation as a U.S. taxpayer living in Switzerland.

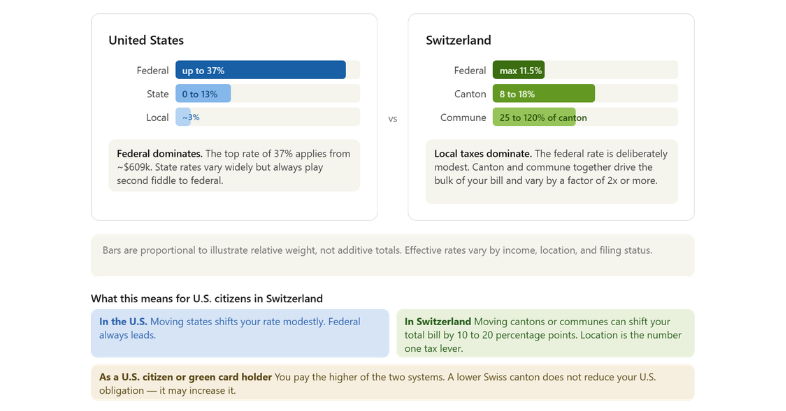

In the U.S., federal taxes are the dominant force, and state taxes are a secondary consideration. Switzerland flips this entirely. The federal Swiss income tax rate is capped at just 11.5 percent, a fraction of the U.S. top rate of 37 percent.

In Switzerland, the real weight of your tax bill is determined by the canton you live in and, within that canton, the specific commune.

This article defines a Swiss canton, breaks down how Switzerland's three-tier tax system works, and explains how canton choice directly impacts your Foreign Tax Credit.

What Is a Swiss Canton?

A Swiss canton is essentially the equivalent of a state in Switzerland. The country is made up of 26 cantons, each with a high degree of autonomy over its own laws, administration, and—most importantly for U.S. expats—its tax system.

While Switzerland has a federal tax framework, cantons set their own income and wealth tax rates, which means your overall tax burden can vary significantly depending on where you live. For Americans living in Switzerland, this makes your choice of canton a key planning consideration. It directly affects how Swiss taxes interact with your ongoing U.S. tax obligations and overall filing strategy, specifically for how much Foreign Tax Credit you can claim and whether you owe anything additional to the IRS.

And there is one rule that applies regardless of which canton you choose: as a U.S. person, you always pay the higher of the two systems. A lower Swiss rate does not eliminate your U.S. obligation. In some cases, it increases it.

Switzerland's Three-Tier Tax System

Unlike the U.S., where most people pay a combination of federal and state taxes, Switzerland operates on three distinct layers: federal, cantonal, and municipal.

Federal taxes are uniform across the country. Everyone in Switzerland pays the same federal income tax rate, which is progressive and capped at 11.5%. This layer is relatively predictable and straightforward.

Cantonal taxes are where the real differences begin. Each of Switzerland's 26 cantons sets its own rates, deductions, allowances, and multipliers. This autonomy means two people earning identical salaries can face effective total rates that differ by 10, 15, or even 20 percentage points simply because one lives in Zug and the other in Geneva.

Municipal surcharges add yet another layer. Each commune applies a multiplier on top of the cantonal amount to fund local schools, roads, and public services. In practice, this means that two neighboring villages in the same canton can have meaningfully different tax rates, sometimes by several percentage points.

The combined effect of these three layers means that where you live in Switzerland matters enormously, both for your Swiss tax liability and for your U.S. filings.

How Cantonal Rates Vary Across All 26 Cantons

The spread between Switzerland's lowest and highest-tax cantons is striking. According to PwC's 2025 cantonal tax comparison, for a single taxpayer earning CHF 100,000, tax rates in cantonal capitals range from as low as 10.20% in the city of Zug to as high as 23.70% in Basel-Stadt, more than double. At higher incomes, the gap widens further: maximum marginal rates at the top end range from 22.20% in Zug to 43.20% in Geneva. That said, your planning priorities will vary dramatically if you are retiring to Switzerland.

Here is a general picture of where the 26 cantons land:

Lower-tax cantons (generally favorable for high earners)

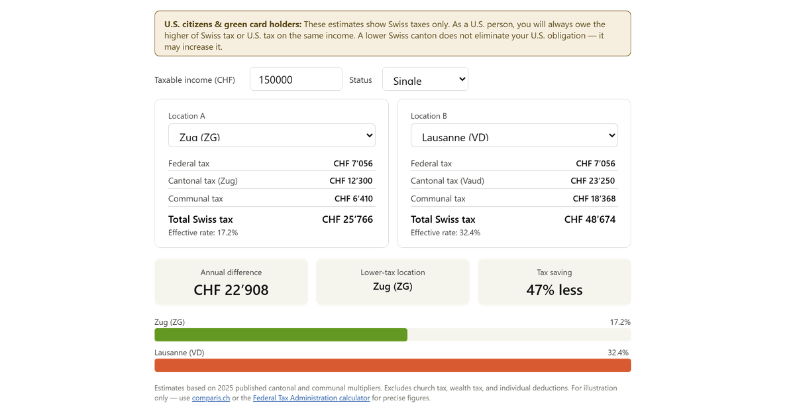

Zug, Schwyz, Nidwalden, Obwalden, Uri, Appenzell Innerrhoden, and Glarus consistently rank among the most competitive. Zug in particular is well-known as a hub for high-net-worth individuals and international businesses. The municipality of Freienbach in Schwyz, for instance, offers a marginal rate of approximately 19.60%, even lower than the city of Zug's cantonal capital rate.

Mid-range cantons

Thurgau, St. Gallen, Graubünden, Aargau, Solothurn, Ticino, Fribourg, and Valais tend to fall in the middle of the spectrum. These cantons often offer a good balance between quality of life and tax burden, and are popular with many expat families.

Higher-tax cantons

Geneva, Vaud, Neuchâtel, Jura, Basel-Stadt, and Bern tend to carry the heaviest tax loads. The city of Geneva, for example, applies a cantonal rate plus a 45.5% communal multiplier, pushing effective marginal rates above 43%. The city of Bern similarly lands at the upper end of the national range.

Even within the same canton, the commune you choose matters. In Canton Vaud, Lausanne carries a higher municipal multiplier than the smaller nearby commune of Lutry, in the same canton, with a different tax bill.

Why Canton Choice Directly Impacts Your U.S. Foreign Tax Credit

As a U.S. citizen or green card holder, you are required to file a U.S. tax return and report your worldwide income regardless of where you live. Switzerland and the United States have a tax treaty designed to prevent double taxation, and most Americans in Switzerland use the Foreign Tax Credit (FTC) filed on IRS Form 1116 as their primary tool for offsetting U.S. tax with Swiss taxes already paid.

The FTC works as a dollar-for-dollar credit: Swiss income taxes paid reduce your U.S. income tax liability on the same income. Here is where your canton becomes directly relevant.

High-tax cantons typically generate a larger FTC

If you live in Geneva or Vaud and your combined federal, cantonal, and communal income tax rate is 35% or higher, you have likely paid more Swiss tax than your U.S. tax liability on that same income. In these cases, the FTC fully offsets your U.S. tax and may even generate excess credits that carry forward up to ten years.

Low-tax cantons may result in additional U.S. tax owed

If you live in Zug or Schwyz and your effective combined Swiss income tax rate is 20% or below, it is possible, particularly at higher income levels, that your Swiss taxes paid do not fully cover your U.S. tax liability on that income. In this scenario, you may owe a top-up payment to the IRS. This is sometimes referred to as a "residual U.S. tax liability" and comes as a surprise to many expats who assumed that living in Switzerland automatically eliminated their U.S. tax burden.

To illustrate

A high-earning U.S. executive living in Zug with an effective combined rate of roughly 22% may still owe additional U.S. federal tax if their American marginal rate is 32% or 37% on that income, since the FTC can only offset up to the U.S. tax owed on that income category.

A similar executive in Geneva, where the combined rate may exceed 40%, would likely have a substantial credit surplus and no additional U.S. liability.

This is one of the most important and most overlooked planning considerations for Americans relocating to Switzerland.

The decision of which canton to call home is not just a lifestyle choice; it has real implications for your annual U.S. tax bill.

Canton Selection as a US-Swiss Cross-Border Tax Planning Decision

The choice of where to live in Switzerland involves many factors, such as proximity to work, schools (if you have kids), quality of life, and cost of living. But for U.S. citizens, it should also involve a deliberate analysis of the cross-border tax implications.

A few key questions to work through with your advisor:

What is your expected Swiss effective tax rate?

The combined federal, cantonal, and communal income tax rate determines how large your Foreign Tax Credit will be. If your effective Swiss rate is below your U.S. marginal rate on the same income, you may owe additional tax to the IRS.

What is your net worth, and how significant is the cantonal wealth tax?

For Americans with substantial assets, the annual wealth tax cost in a high-wealth-tax canton can be meaningful, and generates no U.S. tax benefit in most cases.

Do you itemize on your U.S. return?

If your total itemized deductions (state taxes, mortgage interest, charitable contributions, and potentially the Swiss wealth tax) do not exceed the standard deduction, the wealth tax provides no U.S. tax relief whatsoever.

Are you using the FEIE or the FTC?

Many Americans in Switzerland use the Foreign Tax Credit rather than the Foreign Earned Income Exclusion, because Swiss income taxes typically exceed the U.S. tax on the excluded amount. However, the optimal strategy depends on your income level, the canton you live in, and your broader financial picture. Switching between these approaches has long-term consequences and should not be done without professional guidance.

A Note on Professional Advice

Swiss cantonal taxes interact with U.S. filing obligations in complex ways. The rules around the Foreign Tax Credit, including limitations, income baskets, carry-forward mechanics, and the treatment of wealth taxes, require careful analysis specific to your situation. What works well for a colleague in Zurich may not apply to your circumstances in Geneva or Zug.

At Connected Financial Planning, we specialize in cross-border financial planning for U.S. expats in Switzerland and across Europe. If you are evaluating a move to Switzerland, considering a change of canton, or simply want to ensure your current filing strategy is optimized, we would be glad to help.

This article is intended for general educational purposes only and does not constitute tax or legal advice. Tax rules can change, and individual circumstances vary significantly. Please consult a qualified cross-border tax professional before making decisions based on this content.

Resources

Meet the Author

Arielle Tucker is a Certified Financial Planner™ and IRS Enrolled Agent with Connected Financial Planning. She's spent over a decade working with US expats on US tax and financial planning issues. She is passionate about working with US expats and their families to help secure a financial future that is reflective of their core values. Arielle grew up in New York and has lived throughout the US, Germany, and Switzerland.